- Taxes

Understanding 2026 Income Tax Rates to Create Wealth

I know, you’re busy just trying to make a living, paying that parking ticket, and dealing with that client that’s having a meltdown. But let’s have a quick chat about tax rates. Not sexy, but it’s important.

One of the biggest misunderstandings in personal finance: People think that once their income crosses into a higher tax bracket, all of their income gets taxed at that higher rate.

Nope. Not how it works.

This misunderstanding has cost people real money — and worse, it’s scared them away from earning more.

The income tax system works like a layer cake. Each layer of income has its own tax rate. As your income goes up, only the dollars on that particular layer are taxed at that layer’s rate. The dollars you earned below it? They stay right where they are, at the lower rates. Nobody moves.

Uncle Sam Gives Us the Bottom Layer Tax-Free

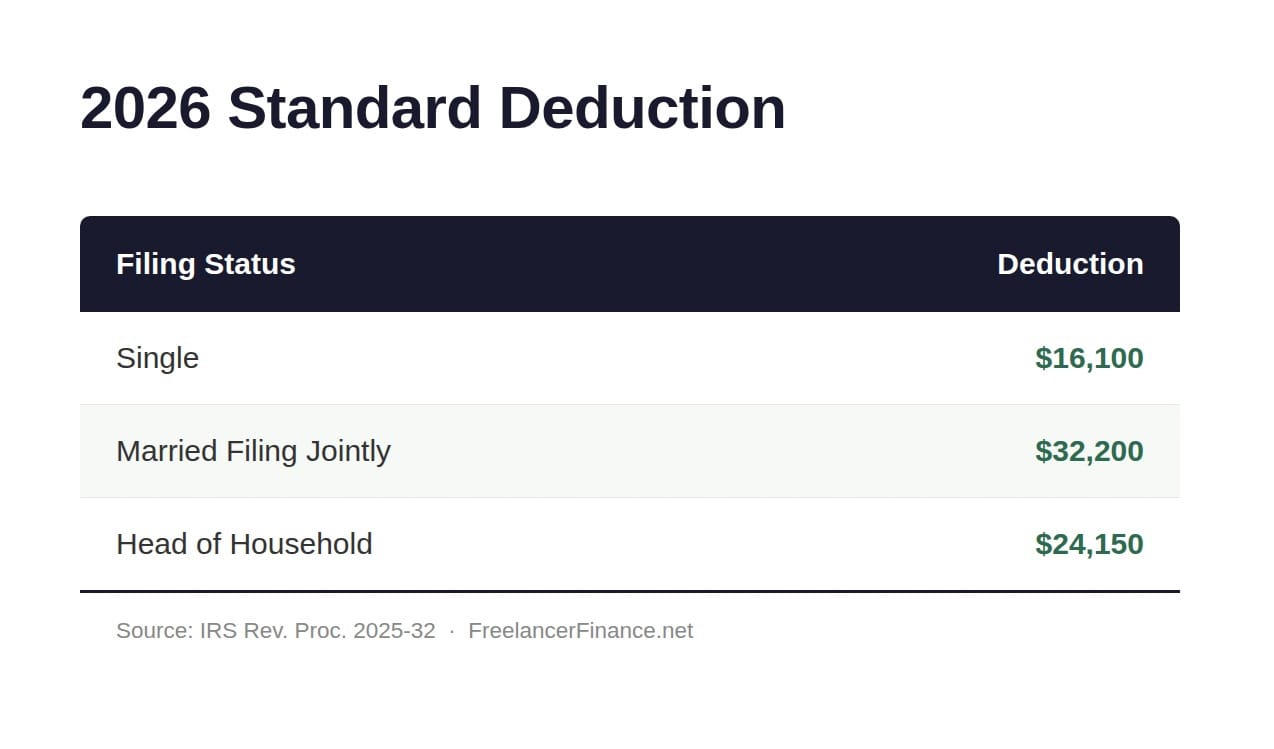

Before the income tax rates take effect, we get to apply the Standard Deduction or Itemized Deduction.

The Standard Deduction: No receipts. No spreadsheet. No tears. The first portion of your income is reduced by a set amount and not taxed at all.

The amount depends on your filing status. After the deduction, the tax rates in the table above begin to apply.

Itemized Deduction: If you think itemizing will add up to more than the Standard Deduction, you itemize. This includes items such as mortgage interest, property taxes, donations, medical expenses (over a threshold amount), and others. These are NOT business expenses; they are calculated elsewhere. Stay with me.

The rule is simple: you pick whichever one is bigger. If your itemized deductions add up to more than the standard deduction, you itemize. If not, you take the standard deduction and save yourself the paperwork.

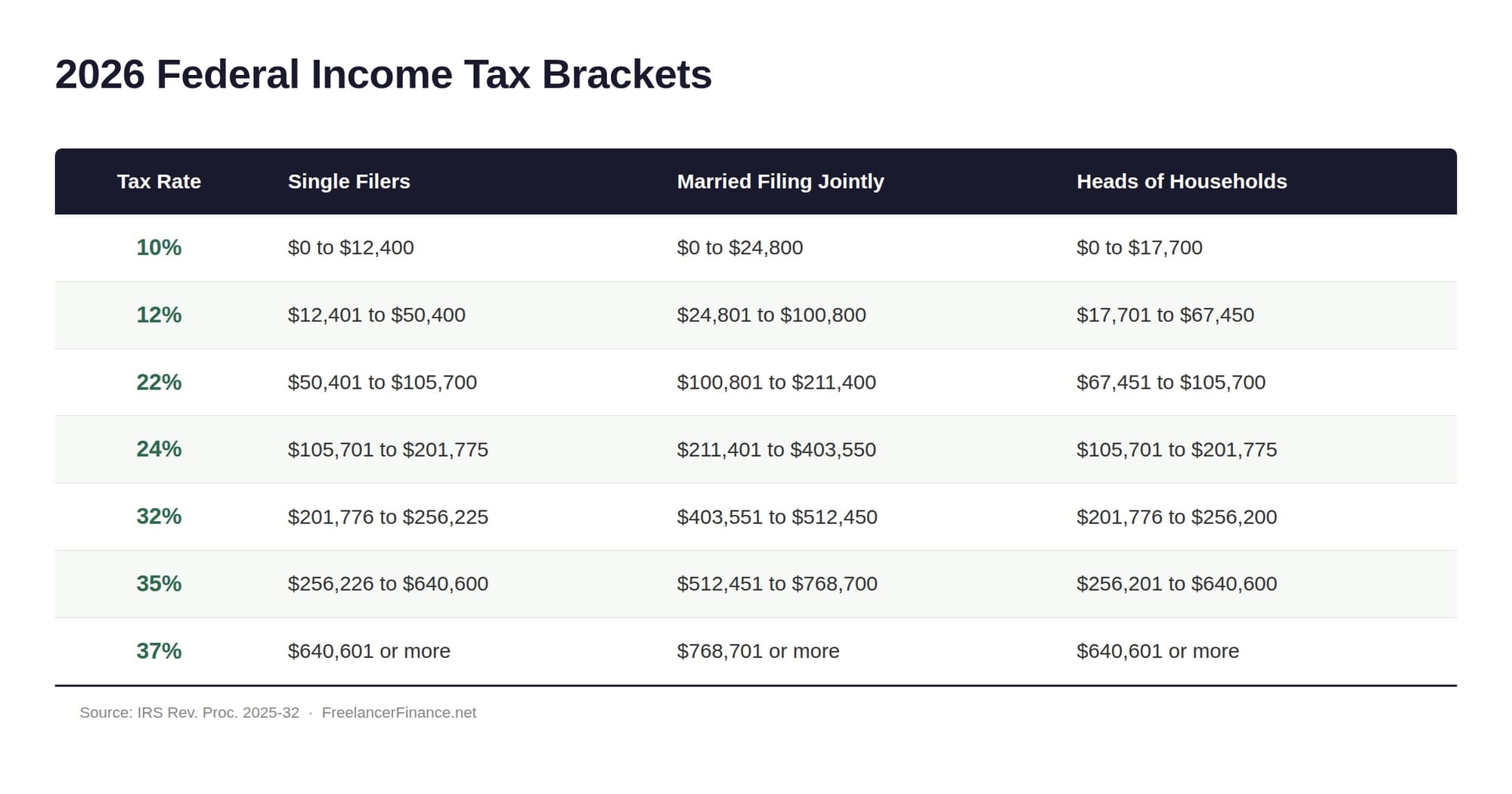

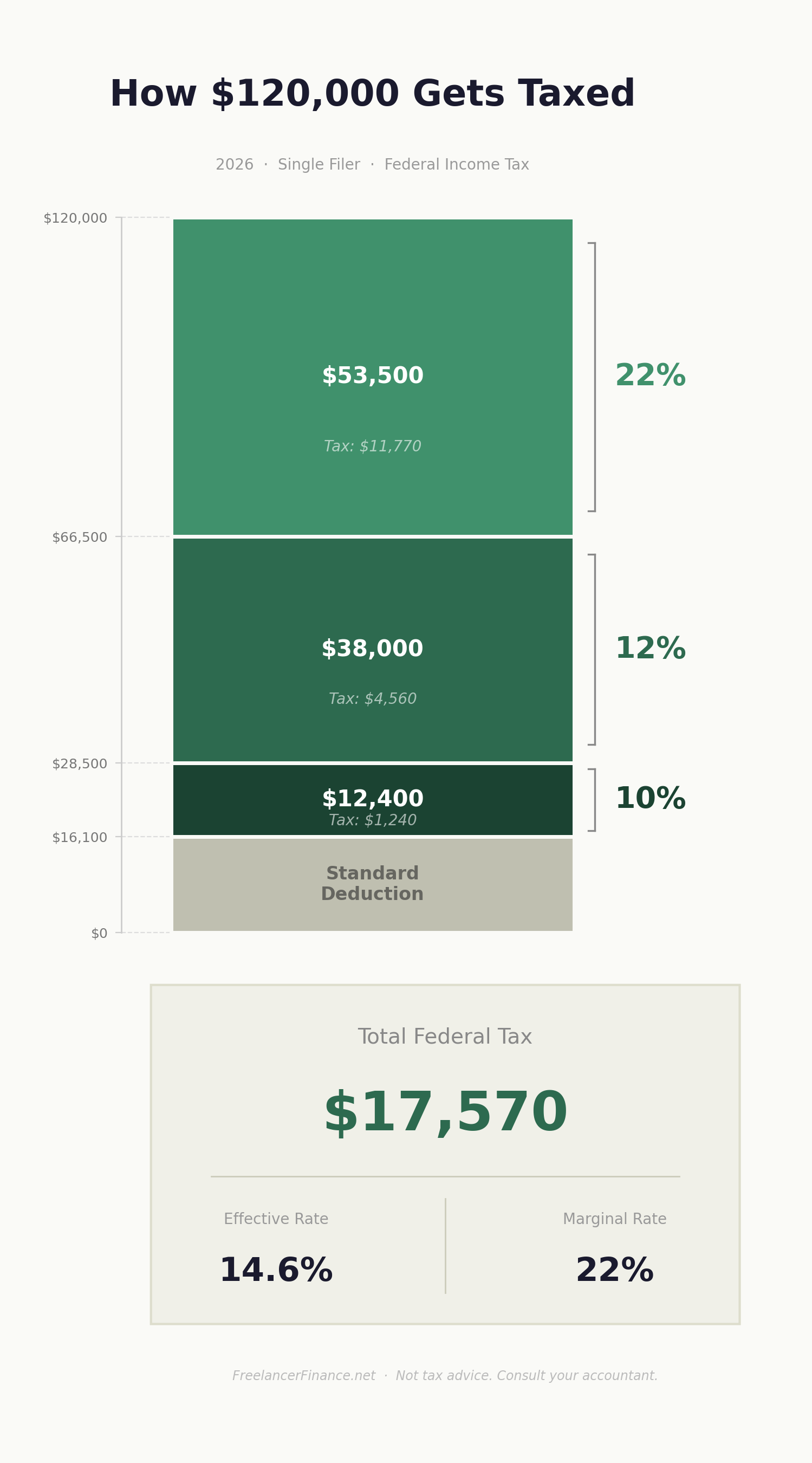

Single and Earned $120,000? Let’s Take a Look.

Here is the ‘income cake’ and income tax rates on each layer if you are filing as single and earned $120k of Taxable Income.

Yes, this looks different compared to the tax rates table above, which starts at $0. That’s because the IRS is referring to your taxable income, which starts AFTER the Standard or Itemized Deduction.

These are the layers:

- The first $16,100 is free if you’re taking the Standard Deduction, then:

- 10% tax on the first $12,400 = $1,240

- 12% tax on the next $38,000 (from $12,401 to $50,400) = $4,560

- 22% tax on the remaining $53,500 (from $50,401 to $103,900) = $11,770

Total federal income tax: $17,570

On $120,000 of gross income, you’re paying $17,570 in federal income tax.

Effective Tax Rate — the actual overall percentage you paid — is 14.6%.

Marginal Tax Rate — the top tax rate you paid — is 22%. But that only hits the last chunk.

This is why earning more money never results in taking home less. You do not pay more tax on your entire income by earning more and moving up into another tax bracket. That myth needs to die. Making more money, means making more money!

You only pay the higher rate on the dollars that cross into the next bracket.

Cut Off the Top of the Cake — How Contributing to Your Pre-Tax Solo 401(k) and HSA Lowers Your Taxes

This is where it gets good. When you contribute to a pre-tax Solo 401(k) or a HSA, you’re cutting income straight off the top of the cake, the highest bracket. The most expensive layer — gone, or at least partially gone.

Using our $120,000 example: Let’s say you put $12,000 into your Solo 401(k):

- You pulled $12,000 out of the 22% bracket ($12,000 × 22% = $2,640). That’s $2,640 of tax you pulled from the jaws of the IRS.

Better yet, that $12,000 you invested in your Solo 401(k) (or IRA + HSA for a freelancer W-2 earner) will grow at an average of around 7%. In 25 years, $12,000 growing at 7% becomes around $68,700. Do that every year for 25 years and you end up with $1.04 million.

Yep. Isn’t compound interest a shocker?

What About State Tax?

If your state has an income tax, it may be a flat tax like Illinois and Colorado. States such as California, New York, and D.C. use the same progressive, layered system as the federal government, but their tax rates and brackets vary by state.

In both cases, contributing to a Solo 401(k) will lower your state taxable income. PA and NJ have some weird rules re: retirement accounts, so watch out for them.

Don’t Forget the HSA

The HSA also qualifies for a tax deduction and can further reduce your taxable income. Use it for medical expenses, or do what I do and use it as an investment account and let it grow. In 2026, you can contribute:

- $4,400 for individuals

- $8,750 for a family

The money stays yours. It’s not use-it-or-lose-it like an FSA. You must have a qualifying health insurance plan.

“I Will Just Buy More Equipment for My Business, So I Pay Less Tax.” Maybe Rethink That.

If you really NEED more equipment for your business to make more revenue, or you’re bringing an equipment purchase forward during a high-earning year, then sure.

Your goal as a business is simple: minimize expenses, maximize profit. Yes, you’ll pay tax on more profits, but it’s your money to keep. Spend a little, invest the rest to create future wealth.

Your Solo 401(k) — The Long Game

Here’s the long game:

By contributing to the Solo 401(k) and HSA, you cut the taxes you had to pay, and your contributions grow untouched by the taxman for decades. You will eventually pay income tax on withdrawals in retirement — but most people earn less in retirement than during their peak earning years. That means your withdrawals will fall into lower tax brackets, and you’ll pay less overall.

The real power? Tax-free, compound growth. Your full contribution grows year after year without getting nibbled at by taxes along the way.

Read more from Chris on his site, Freelancer Finance.